May 2020

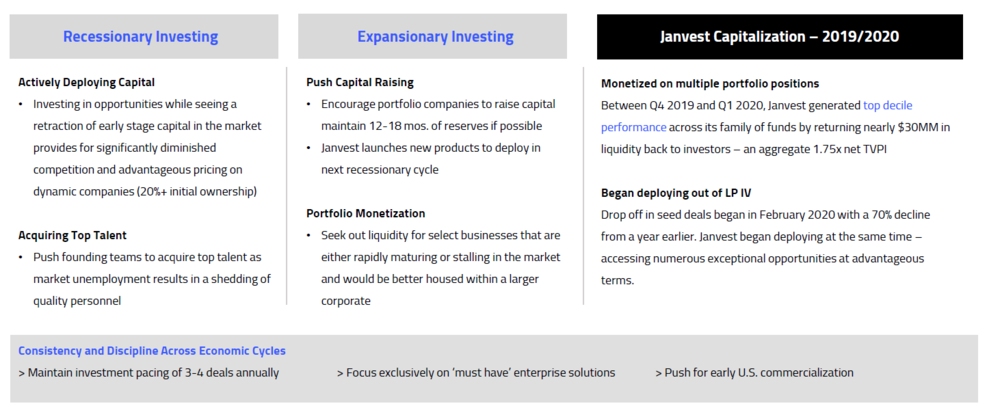

JANVEST ECONOMIC CYCLE MANAGEMENT AND PORTFOLIO POSITIONING

We at Janvest are no strangers to economic downturns. Born on the tail end of the last recession, we have from day one designed our investment and portfolio monetization strategies to be resilient in both expansionary and recessionary periods. When it comes to our ongoing deployment, as well as the strengthening of our legacy assets, we have had a plan in place and are executing accordingly. As it pertains to seed stage investing - fortunes are rarely won or lost overnight. This asset class is a marathon, and if managed appropriately, can be extraordinarily resilient in more volatile markets. Our Economic Cycle Management, highlighted in the graphic below, shows how we approach the ebb and flow of global markets to the benefit of our Limited Partners and portfolio entrepreneurs.

In early 2019, we began stress testing our portfolio companies for a downturn - asking how their current budget, growth projections, hiring plans, infrastructure costs, product roadmap, and capital raising would be affected if sales cycles were elongated, enterprise spending was cut back, and there was a retraction of venture financing. The responses we got ultimately led us to push our portfolio entrepreneurs to prepare for these types of conditions. Today, that strategy has translated into a portfolio that is in a much stronger position than many of our peers.

MARKET CONDITIONS FOR JANVEST DEPLOYMENT

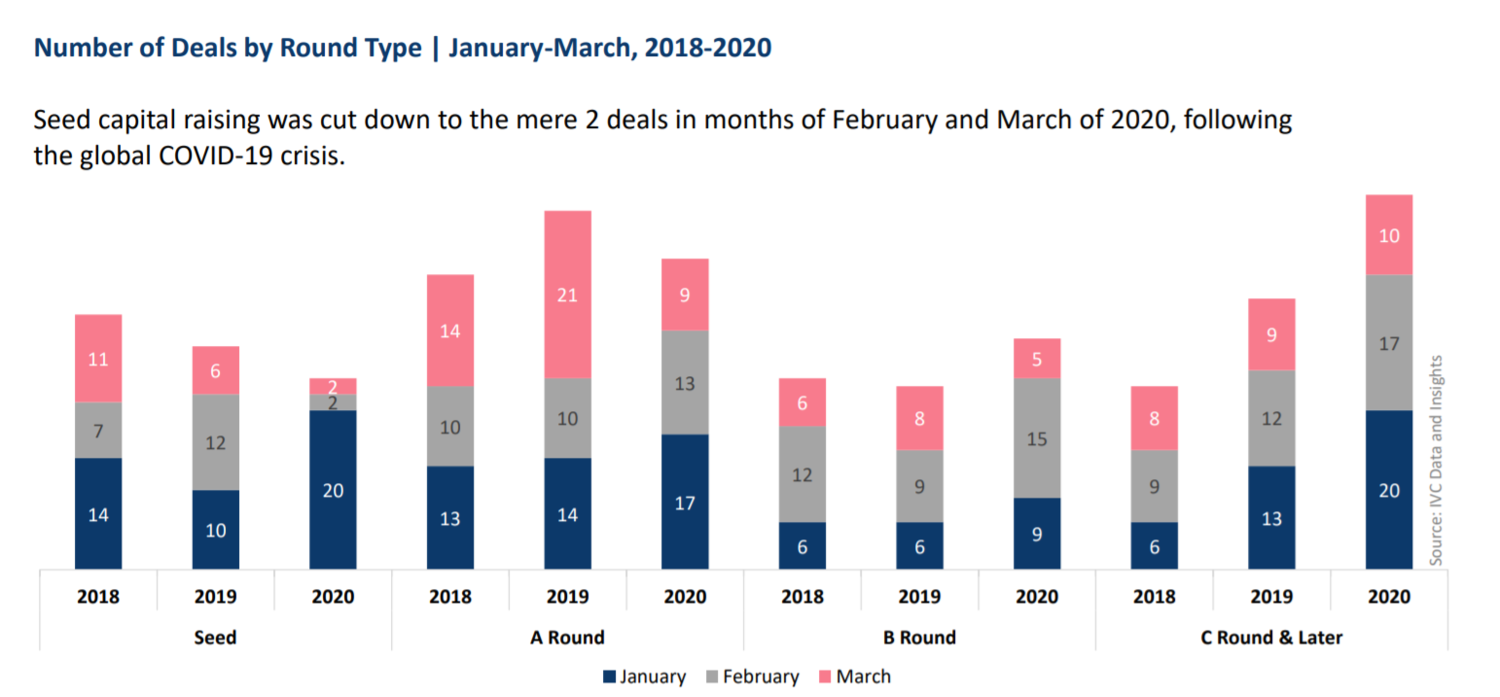

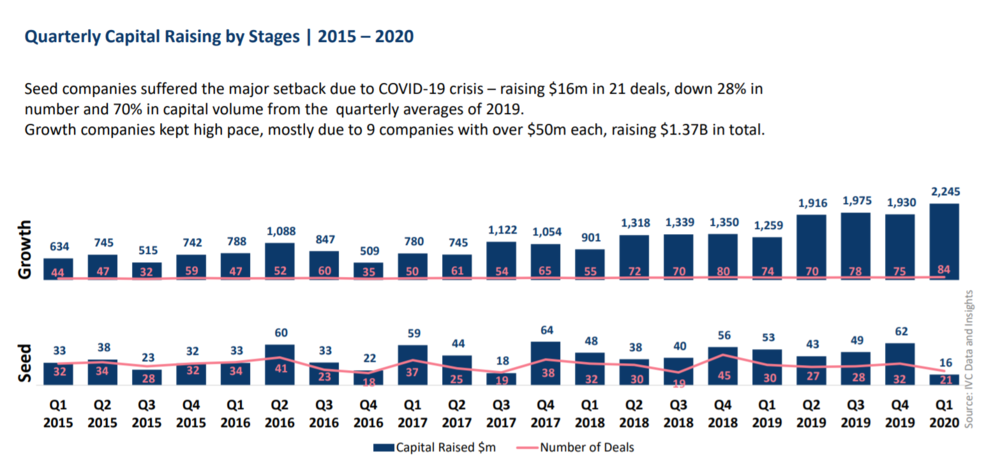

With the rapid onset of this recessionary period, the conditions in Israel have ripened dramatically in favor of early stage investors that have both the capital and appetite to continue investing. In February and March 2020, only four seed deals were reported in Israel representing a 78% decline from the year prior.

In terms of actual capital invested -- in Q1 2020 only $16MM was committed to seed stage companies in Israel representing a 70% decline ($53MM) from a year ago and a 75% decline ($62MM) from just the previous quarter. Despite this dramatic decline in seed deals in Israel, founding teams still need to raise capital to maintain their operations and continue developing their technology. For them this means fewer financing options which translates into more concessions for those willing to finance them.

RECESSIONARY INVESTING AND CAPITAL EFFICIENCY

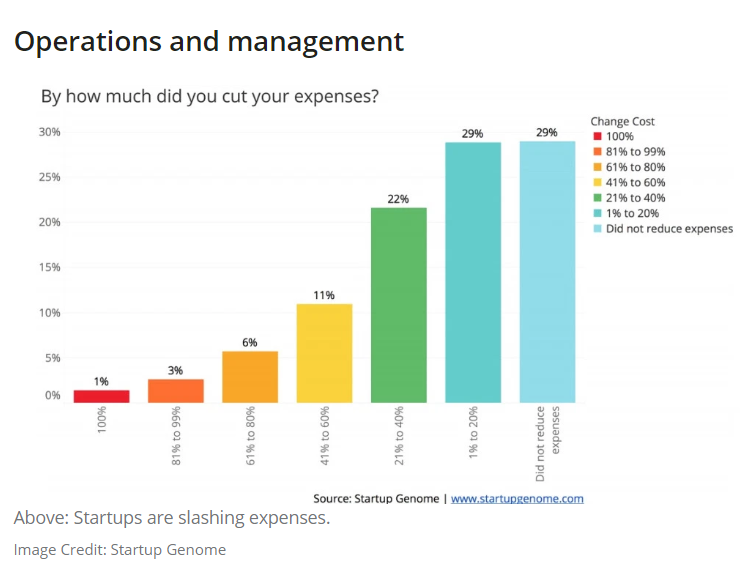

While pre-seed and seed valuations in Israel have seen a correction in the past few months, the biggest adjustment is how efficiently companies are now forced to operate. Prior to COVID-19, many start-ups had a bit of a spending problem - that is, spending an 18 month budget in 12 months because of how readily available capital had become. This meant that start-ups were raising every 12 months rather than every 18-24 months, as is typical. While this truncated time between rounds does wonders for a fund's TVPI (Total Value to Paid in Capital - the unrealized multiple), it sabotages the more important, DPI (Distributions to Paid In Capital - the actual realizations) by forcing that fund to take on additional dilution through the extra 2-3 rounds raised by that company. In a recessionary period, capital is harder to come by and the bar to raise that next round is significantly higher. This translates into start-ups returning to the days of lean operations - taking a $2-3MM seed round and making it last 24+ months in order to achieve the necessary gains prior to an A round. This is already starting to happen. According to a recent study by Start-Up Genome, from March 25th to April 17th 43% of start-ups have cut expenses by more than 20%.

With this capital efficiency not only will companies have lower valuations and thus preferred entry points for investors actively deploying, but they will be forced to extend the periods between funding rounds, limiting unnecessary dilution and turbocharging the eventual economic return. Those investors that choose to optimize around valuation alone (TVPI) will ultimately end up leaving money on the table.

ACTIVE PORTFOLIO UPDATES

At the portfolio level, Janvest's best performing and most promising businesses are well-funded due to successful capital raising campaigns executed in 2019. In addition, given the 'must have' nature of our portfolio technologies, many will continue to thrive in this environment as they provide automation, digitization, and optimization capabilities to enterprises that are looking at ways to cut costs without compromising performance and functionality. Moving forward with these monthly updates, we will provide a 'risk score' for each active portfolio company indicating how 'at risk' that company is from a financing and cash reserve standpoint: LOW RISK, MEDIUM RISK, HIGH RISK

LOW RISK

> Simpo (LP C/SPV III) - raised $15MM in 2019 and in Q1 2020 hit 120% of last year's revenue – currently hiring sales personnel in Silicon Valley

> Coralogix (LP B/SPV III) - raised $10MM in 2019 and secured an additional $3MM in venture debt as a precaution - still expecting at least 100% growth over 2019 even with revised down revenue projections

> Atomation (LP B/LP C) - closed $4MM extension in 2019 and even with revised down revenue projections expects 500% growth in 2020

> Altostra (LP C/SPV III) - closed $3.5MM seed round in 2019 and is using 'downtime' to focus on their product and product-market fit with plans to raise an A round in mid-2021

> Obsecure (LP IV) - closed $1.5MM+ pre-seed round in Q1 2020 and is working on an initial product with plans to raise a seed round in 2021

MEDIUM RISK

> Outgage (LP C) - raised $2MM seed last year and was planning to raise an A round in Q2/Q3 2020 but may see a challenge given a retraction of venture capital - still expecting $2MM+ in revenue in 2020

Mitigation: Janvest is working on an almost daily basis with the CEO to refine her investor materials and to make pointed introductions to relevant VCs here in the U.S.

> Reposify (LP C) - raised $2MM seed last year and was also planning to raise an A in Q2/Q3 2020 but traction wasn't there and the bar for an A has become significantly higher

Mitigation: The Board had Reposify engage an investment banker in February to seek out a strategic buyer of the company. The process has attracted numerous potential acquirers. In the next 8-10 weeks we should know whether this will result in a positive outcome.

> Lingacom (LP B/LP C) - raised $4MM in grants last year from the European Commission and while capital isn't the challenge, the company is experiencing much slower than expected commercialization, which may slow further in a recession

Mitigation: The company may begin exploring a sale of Intellectual Property later in the year if their commercialization opportunities get put on hold into 2021-2022.

HIGH RISK

> ShieldIoT (LP C)- raised $3.6MM seed round last year led by Innogy Ventures and with participation by Janvest which led the company's pre-seed round 18 months earlier. ShieldIoT has had limited success in finding its product-market fit and little chance to raise the next round before they run out of capital later this year.

Mitigation: Janvest is pushing the founders to engage in a tech and team sale process, which could result in a low price point acquisition returning something to the partnership for its investment

FUND LEVEL UPDATES

MONETIZATION

In Q4 2019 and Q1 2020, Janvest was able to monetize on two of its portfolio positions, Presenso and BioCatch, thus returning nearly $30MM in liquidity across our family of funds and providing a multiple across some partnerships while greatly de-risking many of the others.

CAPITAL RAISE FOR LP IV

While the current economic climate did result in a few LP commitments being put on pause for Q2, Janvest LP IV did a $40MM second close on April 1. This allows the fund to continue executing on its planned strategy of leading pre-seed and seed rounds in Israel-based enterprise grade deep technologies. In the coming months, the GP will return to capital raising with the plan to complete its raise by early 2021.

NEW INVESTMENTS

LP IV made its first two investments:

· Obsecure in February where the fund led a $1.5MM pre-seed round

· Rupert in May (to be announced) where the fund led a pre-seed round and then participated in the company’s seed round

The GP will look to continue allocating capital through this period as market conditions in Israel ripen for early stage investors as was addressed earlier in the update.

CAPITAL RESERVES

· LP A – Fully allocated

· LP B – Fully allocated

· LP C – After taking its pro rata in a number of portfolio company financing rounds, the fund maintains approximately 15% of capital to continue investing in the best performers.

· LP D (IV) – Has only allocated $2.35MM of the $40MM committed to date. The fund will reserve up to 50% of its capital for follow-on investments in pre-existing portfolio businesses.

· SPV III – Has deployed 65% of capital – keeping 35% in reserve for follow-on allocations