June 2020

RIGHTSIZING JANVEST IV FOR A POST-COVID ERA

In January 2019 we set out to raise Janvest IV, which would be the culmination of nearly a decade’s worth of best practices from investing in early stage enterprise tech out of Israel. The strategy for this new fund would look much the same as our previous funds in that we would lead early rounds, help the portfolio companies commercialize quickly in the U.S., and drive them towards tier one follow-on financing partners to continue their growth. For this fund we envisioned a partnership of up to $80MM that would allow us to lead $3-5MM seed rounds with $2-3MM checks and have the capacity and ‘dry powder’ to stay with those businesses through their Series C round and perhaps beyond.

On April 1, 2020, we completed a $40MM second close on Janvest IV and made the decision to put the remainder of the raise on ice for a few months to allow for prospective LPs to stabilize from the economic shocks of COVID-19. This ‘pause’ has turned out to be quite good for us as it has provided the ability to finalize a deal we were in the process of executing, better attend to the wave of new deal flow stemming from cash strapped start-ups desperately seeking out capital, and accelerate our due diligence on several promising opportunities. In addition, we also had the chance to talk at length internally about the raise, the affects this pandemic will have on LP appetite, and how the changing market conditions were continuing to ripen in our favor.

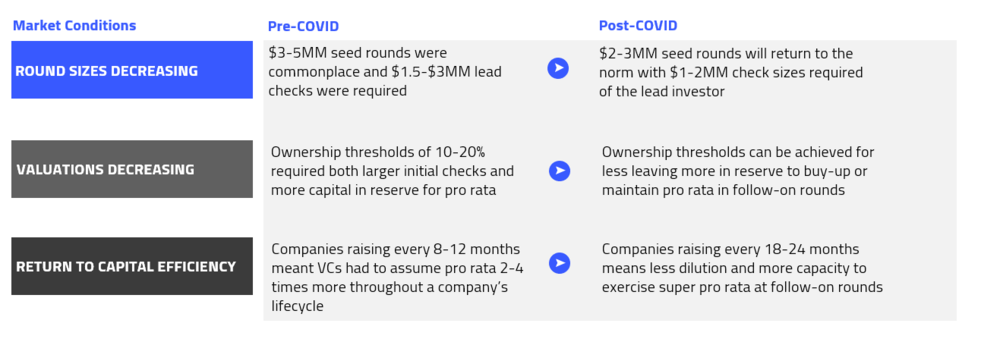

Our conclusion – Janvest IV needed to be ‘rightsized’ for the market, for our investors, and for our strategy. With valuations dropping, round sizes decreasing, competition for great deals declining, and start-up capital efficiency ramping up dramatically, the fact is that our initial $80MM target was significantly more than we needed:

An Oversubscribed $50MM

It is our view that strategy should always dictate the size of the fund, not the other way around as is common with so many in the private equity space. How many checks we want to write, the size of those checks, and the reserves we believe we need to appropriately back our winners are at the core of our fund target. Our decision to ‘rightsize’ the fund is not a retreat from raising the $80MM but rather a correction of LP IV AUM to accommodate the market conditions and supercharge our economic performance. We believe that an oversubscribed $50MM Fund IV will allow us to not only execute fully on our original strategy but do so with greater benefit to our investors.

Ability to more effectively leverage reserve capital

Given the frothiness in the market over the last ten years, many venture funds didn’t really have a reserve strategy. They wrote an initial check and then 12-18 months later wrote another large check to maintain their pro rata in a high-priced up round. While this strategy works for a bull market, it does not fare well in a recessionary period where follow-on capital is not as available and internal investors have to often provide interim or bridge financing without the market validation they had previously. We at Janvest have a track record of picking our winners early, bridging them to their next milestones, and buying up in the process using less capital. Coralogix and BioCatch are just two examples – both needed multiple checks from us before their Series A given the retraction of venture capital in the market. Those interim rounds gave us the ability to use much smaller checks to buy increasingly large stakes in these businesses, which today have provided exceptional results for our investors both from a TVPI and DPI standpoint.

Providing direct access earlier on to “high-flyers”

While even a rightsized Fund IV has the ability to continue to fund the best performers through numerous follow-on rounds, the capacity to take our full pro rata will peak most likely at the Series B. This ultimately means that we have the ability to launch more direct deal SPVs to pass along to our LPs which has always been core to our strategy.

Maintaining appropriate portfolio construction and diversification

Despite a rightsizing, LP IV will still maintain its original strategy of investing in approximately 15 enterprise grade deep technologies with an emphasis on cyber security, data analytics, IoT, business intelligence, Cloud infrastructure, and software.

To the degree LP IV attracts more than $50MM, that additional capital will be added to a ‘super reserve’ that will be used to increase our concentration in the 2-3 absolute best positions in the portfolio without compromising the fund’s original investment or portfolio construction strategy.

As always, we welcome all questions and feedback.