Investment - December 2023

The Joule General Partners are pleased to announce the execution of Limited Partnership IV’s 13th investment in an Israeli founded emerging technology company. Below you will find information about the business and corresponding investment. We welcome your questions and feedback.

DEAL SUMMARY

Company Name / Swish

Website / www.Swish.ai

Offices / Tel Aviv, Israel

Sectors / IT, Artificial Intelligence

Founders / 2

Year Founded / 2018

Number of Board Positions Held by Joule / One

Total Joule LP IV Investment / $2,000,000

Total Size of Round / $5,000,000 (Seed II)

Notable Co-Investors / Dell Technologies Capital, Skywell Ventures, StageOne Ventures, Ariel Maislos

LP IV Ownership / 15.4%

DEAL DYNAMICS

For more than a year we’ve been communicating to our Limited Partners that a dramatic venture market reset was underway. Valuations were declining. Multi-stage funds were pulling back from early stage investing. The bar for subsequent financing rounds was getting higher. And, startups that had over-raised in the last few years during frothier times were going to be scrambling for capital to try and close the gap on valuations that had outpaced their business metrics. To us at Joule, these conditions were not just going to create better pricing and terms for our core seed stage deployment strategy, but we also expected that we were going to see more mature startups willing to accept seed stage pricing in order to survive. This latest Joule IV investment can be characterized as the latter.

In 2018 when Swish was founded, we at Joule had the opportunity to lead the company’s first institutional financing round. Ultimately we declined to invest as we lacked conviction for their market focus at the time. Over the subsequent five years we were periodically in touch with Swish’s CEO as they went on to raise more than $15MM in venture capital from numerous name brand investors. Also in that time, Swish executed multiple business and technology pivots to try and acquire product-market fit. Unfortunately some poor management and product decisions led to limited results until late last year when Swish started to see some interesting and meaningful momentum. Despite acquiring numerous Fortune 1000 customer logos and lining up more than $1MM in annually recurring revenue for 2023, it was too little too late. Swish’s existing investors felt as though new leadership was needed, the company’s valuation was too high to raise new outside capital, the cap table had to be re-balanced, the monthly ‘burn’ was excessive, and there was some outstanding venture debt that was coming due. This list of issues essentially made Swish uninvestable - until the opportunity was presented to Joule.

For 13 years we’ve been dealing with early stage tech assets that come with or run into an array of financial, structural, and governance problems. In fact, two of Joule’s most successful investments, Coralogix and BioCatch, both required recapping and numerous CEO transitions in their early years. Our willingness to roll up our sleeves and put in the work means that we can uniquely turn “distressed” businesses into immensely promising opportunities. To make Swish investment-grade once again, Joule had to create a coalition with the existing shareholders in order to effect the kind of change that would be required. While there was certainly some push-back from those shareholders given the dilutive nature of this round, we made them a part of the pre-round process — collaborating in a way that instilled trust in Joule and encouraged their continued participation in the business (existing investors are committing roughly 40% of the new round). With this coalition, Joule was able to focus on the following overhaul:

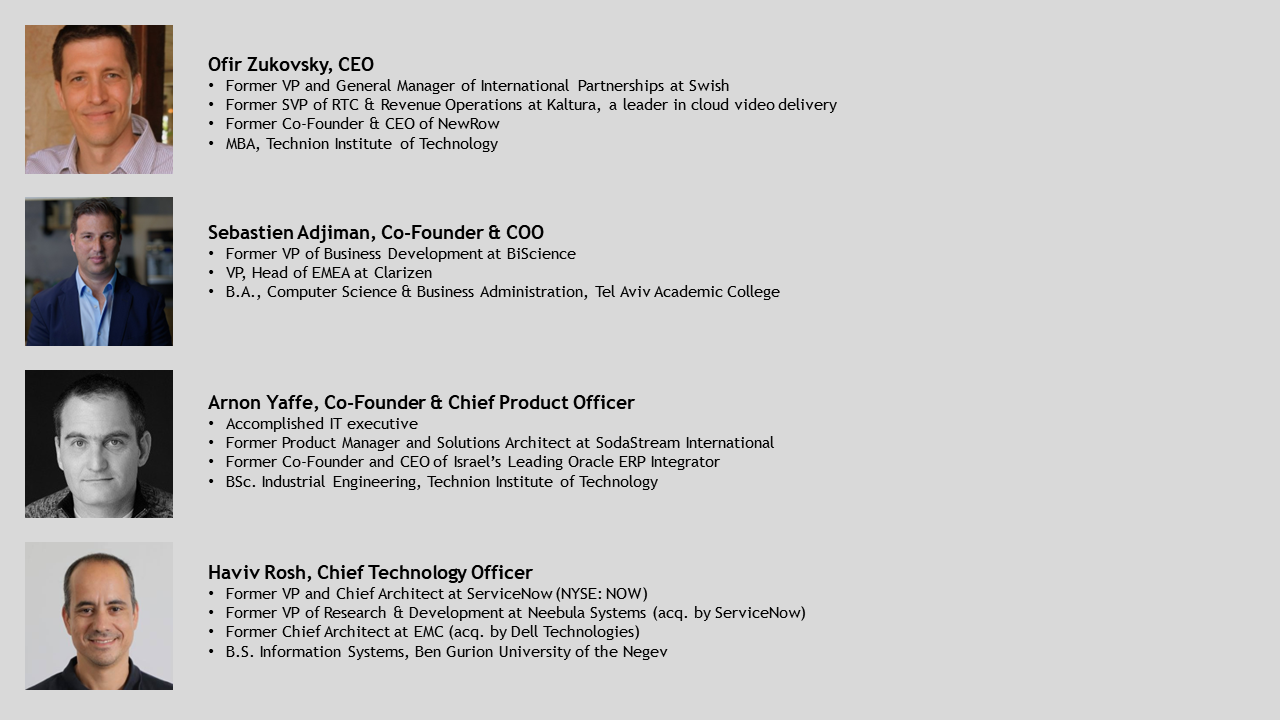

- CEO Transition: As a prerequisite to Joule’s investment, Swish promoted Ofir Zukovsky, VP of International Partnerships and a serial entrepreneur, to CEO. Over the previous year with Swish, Ofir had shown himself to be a talented leader and visionary and, according to the company’s previous Board of Directors, was instrumental in revamping the product and go-to-market strategy that was starting to bear fruit. It is important to mention that we began seriously engaging with Swish in the week prior to the October 7th attack when we realized there would be some significant flexibility on deal terms to incentivize our consideration. Despite Ofir losing extended family members on that day at Kibbutz Beeri he insisted on continuing to be a part of our due diligence process, which spoke volumes about his commitment to the business, his belief in what they are building, and his tremendous character. This type of resilience is precisely what separates Israeli entrepreneurs from their peers abroad.

- Valuation Reset: The valuation of Swish’s last round of financing in 2022 was around $40MM, which was well outside of Joule’s acceptable pricing as a disciplined seed investor. To eliminate the valuation risk, the terms of a new Joule-led deal re-valued the business at around $13MM ($8MM pre-money), essentially re-doing its seed round nearly five years later.

- Business Recap: To re-balance the cap table, Joule needed the new round to buy up most of the business after which more than 50% would be returned to the founders and team via an aggressive Employee Stock Option Plan (ESOP). While Swish’s existing shareholders saw this ESOP allocation as too aggressive, we believe in being overly generous to startup teams, especially in these circumstances, to keep them motivated and committed for the long term.

- Immediate Budget Cuts: Swish needed to re-prioritize capital efficiency - learning how to operate effectively with a fraction of what they spent monthly prior to this Joule-led round. Together with the new CEO, Joule put together a budget that would give the company up to two years of runway with the current financing proceeds and put it in a better position to re-raise a Series A in 8-12 months with a few million in annually recurring revenue.

- Re-Negotiation of Venture Debt Terms: Joule did not want the proceeds of this round to be used to pay off a legacy line of venture debt. If Swish could make good on its revenue projections in 2024, the company could more than afford a monthly debt repayment plan. To achieve this scenario, Joule led a re-negotiation of Swish’s venture debt with the lender, one of Israel’s largest banks, and an institution we’ve worked with closely in the past. These new terms provide Swish with the ability to use this round to accelerate R&D and sales rather than debt repayment.

With most of Swish’s legacy issues resolved and a new financing round completed, the company’s new leadership and Board of Directors can focus on growth without unnecessary distractions.

TECHNOLOGY DESCRIPTION

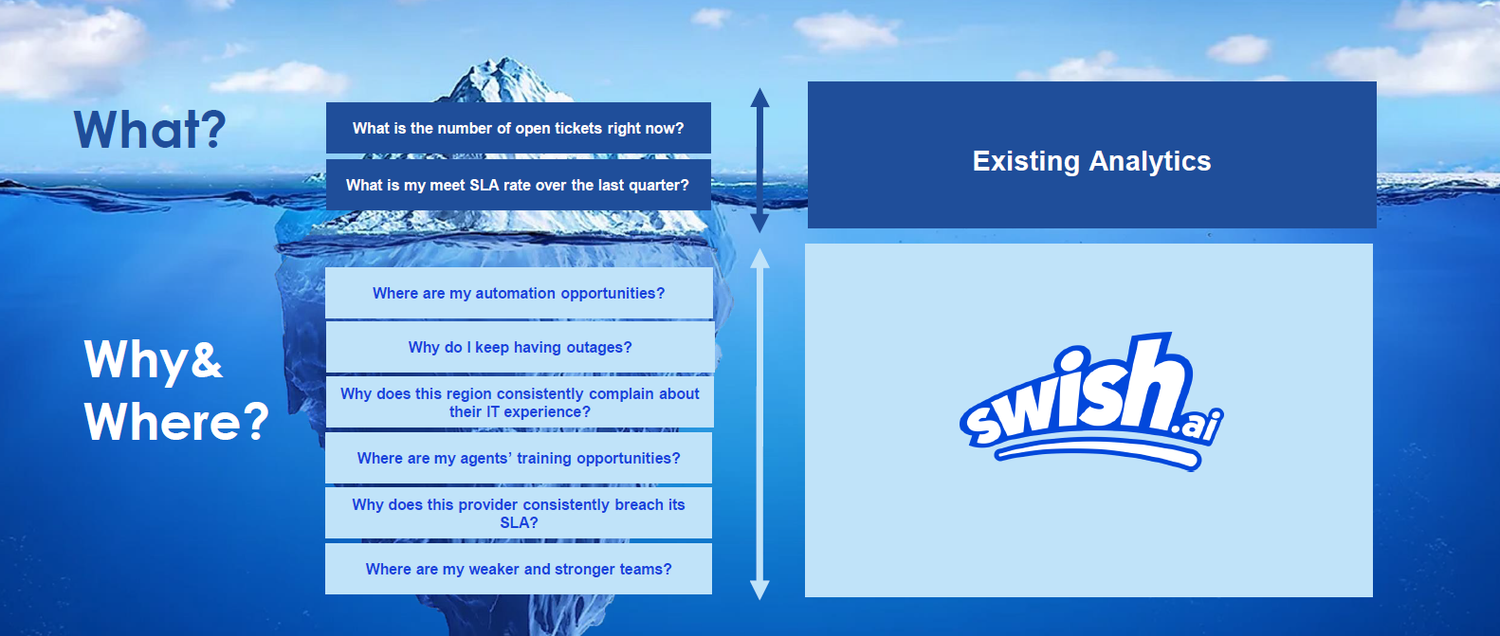

Information Technology Service Management (ITSM) is how IT teams manage the end-to-end delivery of IT services to customers. Contrary to what many believe, IT support is more than just fixing a laptop for an employee or getting someone set up on a file sharing system. In the modern enterprise, ITSM teams oversee a wide variety of workplace technology and mission-critical software applications that impact Human Resources, legal, facilities, marketing, and finance. As more organizations transition to the Cloud, their technology infrastructure becomes more complex with an increasing need to constantly maintain and orchestrate the underlying software. When there is the inevitable software/IT malfunction or user error, tickets are submitted to an organization’s ITSM team as the first step in the (issue) resolution process. For context, just one of Swish’s multi-national customers sees over three million incidences (tickets) on an annual basis.

To meet this growing ITSM demand, companies such as ServiceNow (NYSE: NOW), Atlassian (NASDAQ: TEAM), Freshworks (NASDAQ: FRSH), and BMC (WSE: BMC) are all vying for market share especially amongst the Fortune 5000 and their expansive digital infrastructure. While ITSM is part of a greater Enterprise Service Management (ESM) market, just this ‘niche’ industry is valued at around $9 billion annually with a 9.3% CAGR. The biggest problem with these aforementioned ITSM incumbents is that they were built as a System of Record (SOR) for ticket management and resolution oversight. They were not built for, nor can they operate as a System of Intelligence, which is increasingly valuable to larger organizations. Two other major issues with these Systems of Record: 1) They have tens of millions of users on their systems operating in different languages with company-specific jargon, which makes accurate ‘ticket classification’ (or the clustering of similar/related IT problems) nearly impossible and 2) their software architecture is outdated and ‘heavy’ which limits their ability to quickly process large amounts of data and provide valuable, and much needed, prescriptive insights. Below you can see that what SORs solve for versus what ITSM practitioners require.

Swish is the first to market with a purpose-built IT System of Intelligence that sits on top of these huge ITSM platforms to deliver previously unavailable and undiscoverable analytics and insights that can cut costs and dramatically increase IT operational performance. The company’s AI-based technology automatically and in near real-time turns immense amounts of complex, unstructured, and multi-lingual data into digestible and actionable insights that can:

- Identify anomalous system behavior to predict impending IT errors

- Pinpoint ticket/resolution bottlenecks and areas of inefficiency

- Unlock additional ITSM team capabilities to speed up time-to-ticket resolution

- Alert personnel to IT system instability to ensure business continuity

- Enhance the employee digital experience and cut down on IT servicing needs

Despite spending millions annually on these IT Systems of Record, Swish’s customers rave about the added value they get from their platform. The ITSM team at Allianz, one of the largest insurance companies in the world and a fairly new Swish customer, handles roughly 250,000 IT incidences a month. Their System of Record, ServiceNow, can only handle up to 50,000 incidences a month, which means there is a constant backlog of tickets needing resolution with no way to enable effective ticket classification. In addition, Allianz has 6,000 teams globally that have different IT issues with different process owners, business owners, and help desk managers. ServiceNow cannot keep up and is creating a real drag on Allianz’s ITSM efficiency. Swish on the other hand can ingest a near-infinite number of incidences at a time, immediately translate them to English, learn each team’s unique company lingo, effectively categorize the incidences, cluster them to be able to solve multiple tickets simultaneously, and then deliver corresponding prescriptive insights. According to Allianz’s ITSM Lead, “They (Swish) don’t provide a dashboard - they provide an analytics platform that allows us to turn issues into actions.” Whereas SOR customer implementations can take 6-8 months and cost between $30,000 and $60,000, Swish can be up and running at a fraction of the cost and in 2-4 weeks. This “quick” time-to-value is a meaningful motivator for ITSM practitioners who are already overloaded and want solutions that are light, effective, and require a minimal time commitment.

It is important to note that Swish’s solution is SOR agnostic, which means it works on top of all of the leading ITSM platforms. And, while Swish is currently focused on the ITSM market, their goal is to expand their value proposition to other ESM arenas, each of which is a multi-billion dollar category.

MARKET ADOPTION

Despite some sub-optimal management and product-related decisions early on in the company’s life, Swish started to see some initial momentum in 2022 in terms of customer acquisition and revenue growth, especially amongst Fortune 5000 IT and ITSM departments, which have both the greatest need and corresponding budget. Below are a sampling of Swish’s customers, as well as some data around their business metrics:

- $1,100,000: Projected 2023 ARR

- $5,000,000: Projected 2024 ARR ($18M pipeline)

- $77,000: Average ARR per Customer ($250K Avg. Expansion Opp.)

- 80%: Steady State Gross Margin

- 100%: Net Revenue Retention

EXECUTIVE TEAM

As mentioned previously, a leadership transition was a prerequisite for this round. Fortunately, there was an exceptional and proven talent already within the company that allowed us to promote internally rather than make a ‘leap of faith’ external hire.

JOULE VALUE-ADD

Joule put in considerable time and effort into rectifying many of Swish’s legacy problems that inhibited its growth and capital raising efforts, as was previously mentioned in this announcement. If not for Joule making these necessary changes and having conviction around the opportunity, this business would be shutting down by end of year. Giving Swish this new ‘lease on life’ and doing so through an efficient, transparent, and collaborative due diligence and negotiation process has acquired considerable loyalty and appreciation from the founders and team that we expect to pay dividends as they grow.