Investment - April 2025

DEAL SUMMARY

Company Name / Cache

Website / https://mycache.ai/

Offices / New York City & Tel Aviv, Israel

Sectors / Financial Technology, Artificial Intelligence

Founders / 2

Year Founded / 2023

Number of Board Positions Held by Joule / One

Total Joule LP V Investment / $2,000,000

Total Size of Round / $4,000,000 (Seed)

Notable Co-Investors / Mucker Capital (Los Angeles), Bullet Ventures (NYC)

LP V Ownership / 12.0%

DEAL DYNAMICS

Joule's New York-based Partner, Daniel Frankenstein, had an existing multi-year relationship with Cache CEO Dr. Liran Eliner, also a NYC resident - a connection made through Avi Turgeman, CEO of Joule-backed Ironvest and the former Co-Founder and CTO of BioCatch, which the firm seeded in 2011 out of Fund I. The initial iteration of Cache was built as a platform selling direct to consumers that would automate personal financial management. While the technology was groundbreaking, the company's B2C model did not fit our enterprise strategy and so we declined to invest as Cache got its start. During the company's first year, Dr. Eliner regularly consulted with Daniel on issues related to their business and their B2C go-to-market efforts. While the vision was good and consumers indicated that they clearly wanted the kind of automation Cache was building, they lacked confidence and trust in its delivery via a third party application. To deliver that confidence, Cache started packaging their technology up for banks and credit unions to then white label and provide to their customers. The early validation for this new direction received an overwhelmingly positive response from decision makers amongst blue chip American financial institutions. With Cache's new enterprise focus, combined with Dr. Eliner's domain expertise as a PhD from Harvard with a dissertation on the behavior of retail investors, and the existence of a trusted relationship between our two organizations, Joule jumped as a first mover to lead the company's seed round. Daniel will represent Joule on Cache's Board of Directors.

TECHNOLOGY DESCRIPTION

The world of retail banking is evolving. Competition for deposits is increasing. Consumers are spreading out accounts across more financial institutions. Service charges and fees are getting rolled back. Younger clients are harder to attract. And competition from big tech and financial technology companies are eating into market share. As such, banks are under more pressure to innovate. As part of his PhD at Harvard, Cache CEO Liran Eliner interviewed more than 2,000 retail banking customers and discovered that day-to-day money management is one of the biggest headaches for consumers when it comes to their personal finances. Other findings from Dr. Eliner's research:

The average middle class family has between 30-40 financial accounts with no way to keep track of them

90% of consumers don't repay their credit cards by APR, costing on average $1,500 a year per card

79% of consumers don't have a high yield savings account, costing up to $1,200 a year per person

47% of consumers forget to withdraw all their FSA funds by end of year, costing $500 on average per account

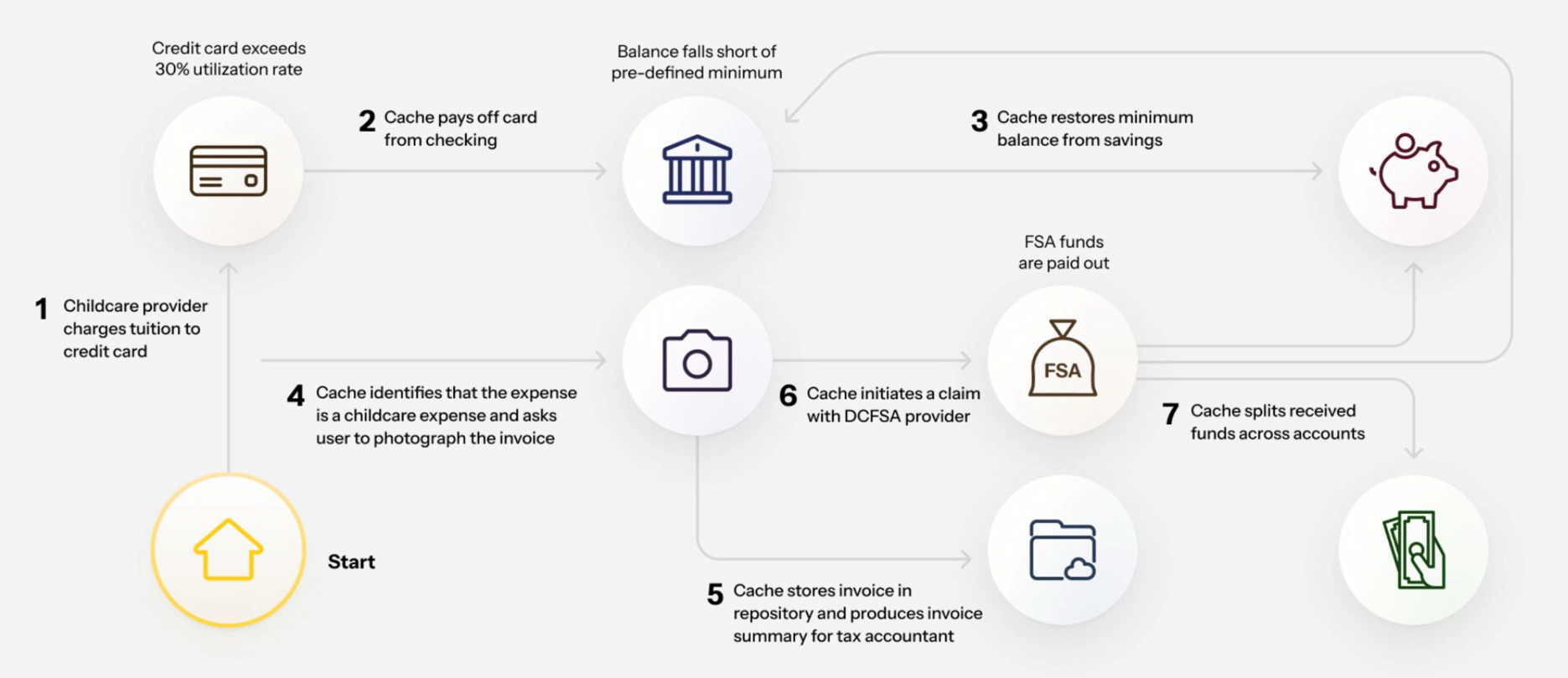

Cache wants to enable banks to transform from 'money holders' to 'money managers'. Instead of trying to change consumer behavior, which Cache's predecessors have tried to do unsuccessfully, Cache is aiming to embrace consumer behavior by injecting automation into the 1-2 minutes a day each person spends on their personal finances. In a bank sponsored 'Cache ecosystem' money deposted into accounts would be automatically routed to service debt, accrue interest, and add to savings in the most efficient and cost effective way. For the average retail banking customer (those without assets actively managed by a wealth advisor) the following workflow is an example of Cache's system at work (click to enlarge):

However, Cache's value proposition extends far beyond automated cash management for bank customers, which is what excites these financial institutions the most. Right now banks have limited visibility into the full financial picture of their customers. As banks begin to roll Cache out to their customers, those customers will connect more of their external financial institutions to extract the maximum value out of the system and it's autonomous, cost effective money movement and debt servicing capabilities. With those external APIs connected to Cache, banks will have a full view of accounts across other institutions enabling them to upsell individually-tailored products and improve underwriting. This type of insight and data is 'gold' for banks and allows them to generate new streams of revenue off existing customers knowing what solutions they need at the right time.

From an addressable market standpoint, the global bank automation and Artificial Intelligence market is estimated to be valued at $33 billion a year with the expectation that it will grow to nearly $230 billion annually by 2034. As more consumers shift exclusively to digital banking, financial institutions will be required to innovate in terms of personalization, product differentation, easy to use interfaces, automated functionality, and so on. Cache can play a central role in helping banks continue to transform into 21st century financial partners to consumers.

MARKET ADOPTION

Despite the notoriously long sales cycles associated with selling into financial institutions, Cache has done an exceptional job at making quick in-roads to an array of banks, credit unions, and credit bureaus to line up a healthy pipeline of prospective customers that are expected to produce up to $3 million in annually recurring revenue in 2025.

EXECUTIVE TEAM

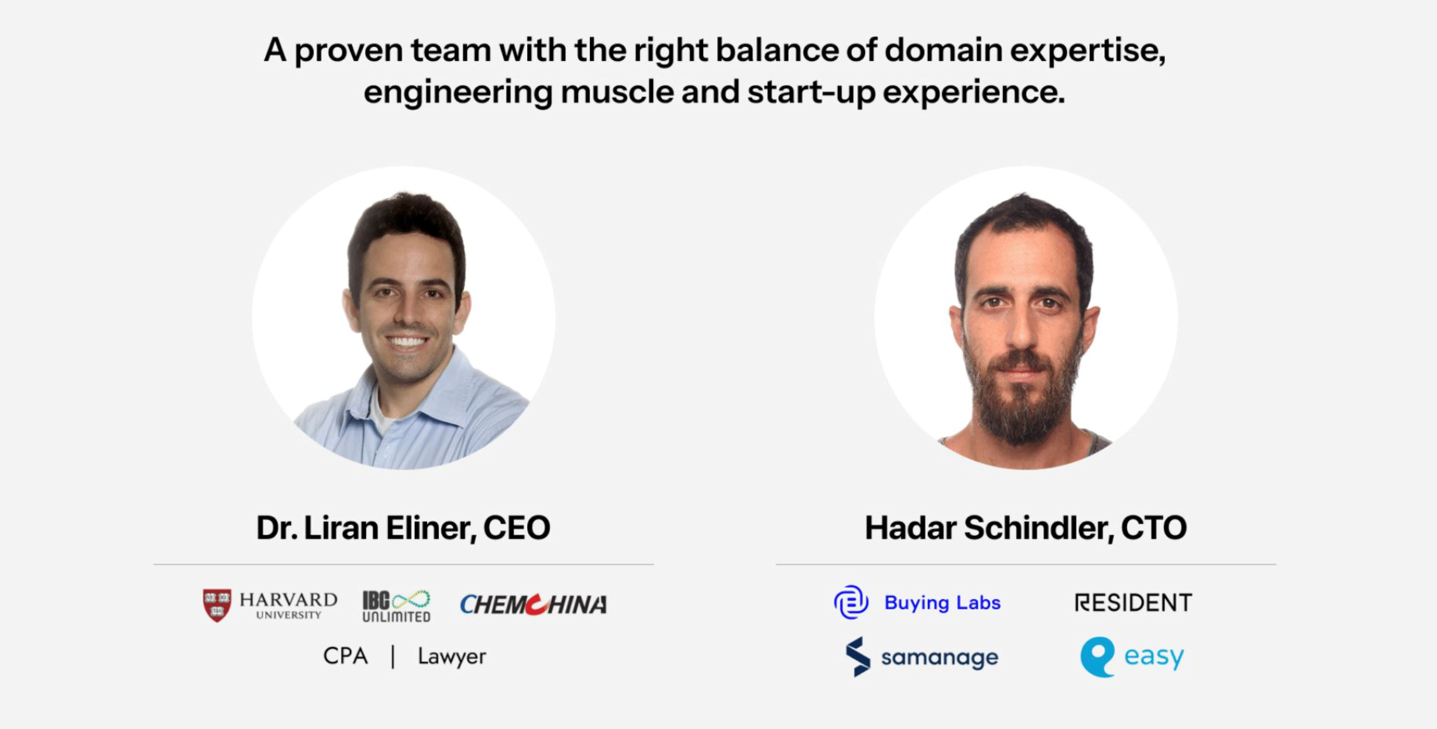

CEO Dr. Liran Eliner spent nearly five years in the Israeli military achieving the rank of captain before getting his law degree at Tel Aviv University. He clerked for the Supreme Court of Israel and then joined The Israel Securities Authority as a Corporate Finance Director. He served as M&A and Strategy Advisor to numerous bi-national companies and most recently completed his PhD through a joint program at Harvard's Business School and Graduate School of Arts and Sciences.

CTO Hadar Schindler has a degree in Electrical and Computer Engineering from Ben-Gurion University of the Negev in Israel and has served in a variety of software development roles throughout his career, most notably as Director of Engineering at Resident, which Ashley Homes acquired for $1 billion last year. Hadar is an expert in the deployment of Artificial Intelligence and Large Language Model deployment and splits his time between Hamburg, Germany and Tel Aviv, Israel.

JOULE VALUE-ADD

As is expected in our due diligence process, we facilitated introductions to numerous prospective customers that also served as validation for us with leading U.S. financial institutions. Amongst those introductions included Truist (NYSE: TFC), NCR (NYSE: VYX), and Vystar Credit Union, one of the fastest growing credit unions in the country. In fact, Vystar was so impressed with the value proposition that the SVP of Payments who oversees all movement of money within their organization, stopped Dr. Eliner midway through the pitch and suggested they move forward with an NDA and a discussion on a scope of work to get started.

In addition, Joule led an effort to relieve the company of some painful terms that had been incorporated at the pre-seed round that could come back to harm the company at later rounds. This process acquired significant appreciation from the Cache team and will help position the company for a successful Series A financing.